ARCHITECTURAL BRIEFING 004

ARCHITECTURAL BRIEFING 004

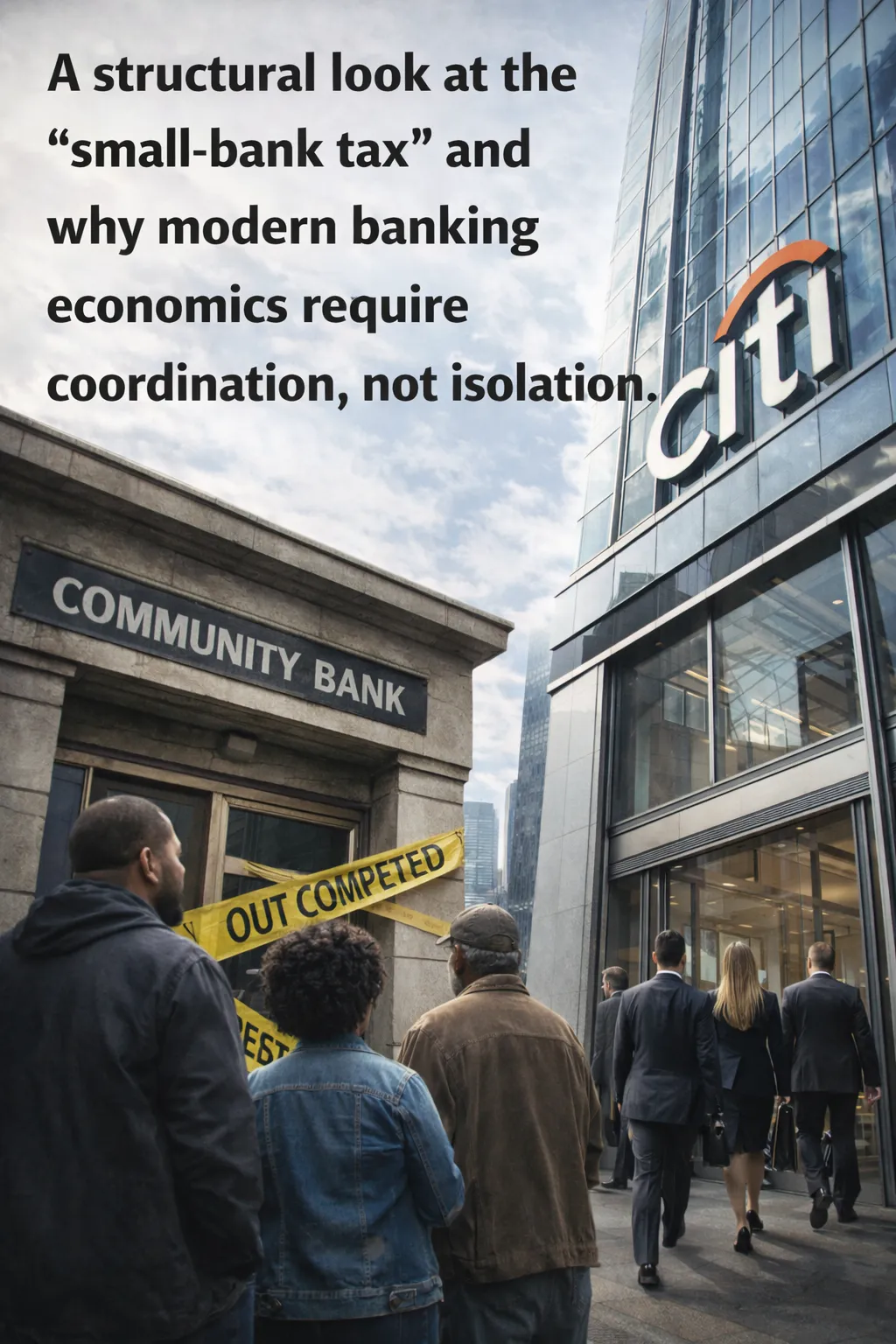

The Small-Bank Tax: Why Consolidation and Shared Services Are No Longer Optional

Community banks do not compete on a level playing field.

They operate under a permanent cost disadvantage that compounds over time regardless of intent, mission, or loyalty.

This disadvantage is not ideological.

It is structural.

And for Black-owned banks, it is amplified.

What the “Small-Bank Tax” Actually Is

The small-bank tax is the cumulative burden imposed on institutions without scale.

It manifests as:

fixed compliance costs that do not scale down,

cybersecurity and fraud requirements that grow annually,

core banking systems priced for volume,

regulatory expectations identical to larger peers,

and vendor relationships negotiated without leverage.

These costs are unavoidable.

They are incurred whether a bank has $300 million in assets or $30 billion.

For smaller institutions, this means:

margins compress faster,

innovation slows,

and strategic flexibility erodes.

Survival becomes the priority.

Growth becomes the risk.

Why Mission Does Not Offset Cost

Many Black-owned banks are expected to serve as:

community lenders,

cultural symbols,

and financial first responders.

These expectations are rarely paired with the capital, infrastructure, or scale required to support them.

Mission does not lower compliance costs.

Representation does not reduce cybersecurity exposure.

Sentiment does not modernize core systems.

Banks that attempt to carry institutional responsibility without institutional resources absorb the penalty directly on their balance sheets.

The False Independence Narrative

Independence is often treated as a virtue in community banking.

In reality, isolated independence is expensive.

Historically, banking power has grown through:

consolidation,

shared infrastructure,

and strategic partnerships.

No modern banking system can scale by remaining fragmented.

Fragmentation increases cost.

Coordination reduces it.

This is not a loss of identity.

It is a gain in capacity.

Shared Services as a Scale Multiplier

Shared services are not a compromise.

They are a strategy.

A shared-services model allows institutions to:

centralize compliance tooling,

pool cybersecurity resources,

share underwriting expertise,

negotiate better vendor pricing,

and accelerate technology adoption.

This model does not eliminate independence.

It preserves it by making independence viable.

In other sectors, shared services are standard.

In banking, they are increasingly unavoidable.

Why Consolidation Must Be Reframed

Consolidation is often perceived as failure or surrender.

In reality, consolidation is how:

capital is preserved,

talent is concentrated,

and institutions survive generational transitions.

For Black-owned banks, consolidation must be reframed as:

a tool for resilience,

not an admission of weakness.

The alternative is permanent smallness and permanent exposure to the small-bank tax.

The Strategic Choice Ahead

The choice is not:

independence or growth.

The choice is:

coordinated strength or isolated vulnerability.

Banks that remain small must:

accept narrower product menus,

slower modernization,

and higher relative costs.

Banks that coordinate can:

expand business banking capabilities,

improve regulatory posture,

and create pathways to scale that individuals cannot achieve alone.

Implications for Bank Ownership

Any serious pathway to Black bank ownership must address the small-bank tax directly.

Ownership without scale inherits the penalty.

Ownership with coordination reduces it.

Consolidation and shared services are not future considerations.

They are present requirements.

Closing

The small-bank tax is not imposed by regulators alone.

It is imposed by the economics of modern banking.

Institutions that ignore it pay indefinitely.

Institutions that design around it endure.

The question is not whether consolidation and shared services will occur.

The question is whether they will occur deliberately or under pressure.

Keystone Black Capital

Capital Intelligence for Ownership & Institutional Design

Architectural Briefing No. 004

Receive new research the day it publishes. Subscribe →