COMMUNITY INTELLIGENCE 007

COMMUNITY INTELLIGENCE 007

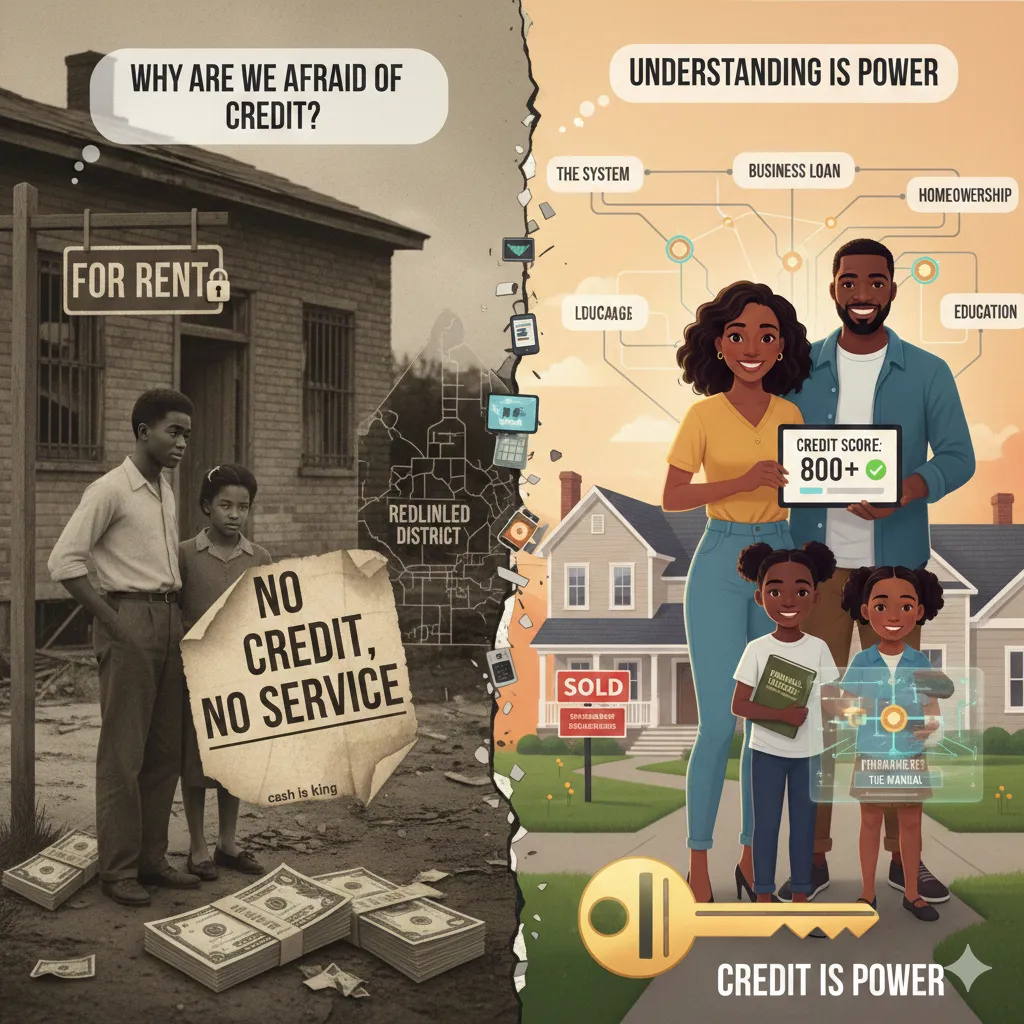

Why Are We Afraid of Credit?

There is a hard truth about money in America that most people are never taught:

People who build wealth do not do it by avoiding credit. They do it by understanding how to use it.

Credit is not just a financial product. It is an operating system. And the Black community was never given the manual.

What Many Black Households Were Taught

For generations, the message was clear and consistent: Work hard, save your money, avoid debt, don’t owe anyone, and stay out of trouble

That guidance wasn’t foolish. It was protective.

At a time when credit was routinely denied, weaponized, or offered under predatory terms, avoidance was rational. Cash meant safety. Debt meant risk. Owing meant vulnerability.

But the system evolved. The instructions did not.

This is not about discipline. It is not about values. It is about education and exposure.

What Credit Actually Is

Most people misunderstand credit because it’s taught emotionally, not structurally.

Credit is not money. Credit is permission. Permission to borrow at lower cost, rent or buy in certain neighborhoods, start a business without paying everything upfront, absorb emergencies without total collapse, and leverage time instead of trading labor endlessly.

Credit is a reputation system institutions use to answer one question:

“How safe are you to do business with?”

That judgment often follows you more closely than your income, your degree, or your effort.

What Good Credit Actually Enables

When credit is understood and managed correctly, it quietly changes the economics of life:

Lower interest rates make everything cheaper

Housing options expand

Business and investment capital becomes accessible

Liquidity exists during emergencies

Assets can be acquired without waiting decades

This is why someone earning less, but using credit strategically, can move faster than someone earning more who avoids it entirely.

Wealth is not just about how much you make. It’s about how efficiently you can deploy capital.

Why Credit Feels Dangerous in the Black Community

This fear did not come from ignorance. It came from experience.

Historically, credit was denied through redlining or offered through predatory structures or punished more severely when mistakes were made.

Over time, credit became associated with stress, shame, loss, and generational damage.

That fear was learned. And it was rational.But rational fear can still become a long-term disadvantage.

Warnings Were Passed Down; Not Instructions

Many of us grew up hearing:

“Don’t owe nobody.”

“Cash is king.”

“Debt will ruin your life.”

What we rarely heard:

how credit scores actually work

why utilization matters

how leverage is used intentionally

how mistakes are repaired, not fatal

When education is missing, fear fills the gap.

Avoidance becomes the strategy. Not because it’s optimal, but because it feels safe.

How Credit Is Often Taught Differently Elsewhere

In many white households, credit is introduced early and treated neutrally.

Children are more likely to be added as authorized users; see mortgages as normal; understand that mistakes are fixable.

Credit is not moralized. It is not tied to character. It is treated like a tool.

The question is never: “Should I use credit?”

It’s: “How do I use it well?”

That difference compounds over decades.

Early Experiences Shape Everything

For many Black adults, first encounters with credit looked like:

store cards with 28–30% interest

overdraft fees

medical debt

payday loans disguised as assistance

That teaches your nervous system to associate credit with danger.

Layer on:

denials without explanation

hidden fees

different treatment by name or zip code

Avoidance begins to feel like protection.

The Hidden Cost of Avoidance

Avoiding credit in a credit-based economy does not make life safer. It makes life more expensive.

It leads to fewer housing options, harder paths to entrepreneurship, emergencies becoming disasters, slower wealth accumulation, and dependence on cash and labor.

This creates a cycle:

limited credit → higher costs

higher costs → slower progress

slower progress → reinforced fear

It feels responsible but it isn’t.

What’s Actually Missing: Literacy, Not Character

The gap is not responsibility. It’s normalization and instruction.

Other communities were not inherently better with money. They simply learned the system earlier and with fewer consequences.

Credit education:

replaces fear with strategy

turns income into leverage

reveals bad deals before they trap you

creates options instead of limitations

Education is protection.

Why This Must Be Collective

When only a few people understand credit:

progress is slow

mistakes are expensive

fear stays unchallenged

When knowledge spreads:

conversations become practical

children inherit structure

norms begin to shift

That is how financial behavior actually changes—not through shame, but through shared literacy.

The Mindset Shift That Matters

Old thinking: Avoid debt.

Better thinking: Learn the rules.

Old belief: Credit is dangerous.

Reality: Ignorance is expensive.

Old strategy: Pay cash to stay safe.

Truth: Cash without credit limits your future.

This Is Bigger Than Money

This is about housing security, ownership, independence, legacy, and control.

Credit literacy is institutional literacy. And literacy is power.

Final Truth

The old narrative says Black people are bad with money. The honest one says we were never taught how the system actually works. And systems do not reward good intentions. They reward understanding.

Avoiding credit does not protect you in a credit-based economy. It makes you invisible. And invisibility costs more than interest ever will.

Receive new research the day it publishes. Subscribe →